Eurocell’s full year 2025 results arrive against one of the most challenging backdrops the UK fenestration and wider construction supply chain has faced in recent years. Weak housing activity, subdued RMI demand and persistent macroeconomic uncertainty have constrained volume growth across the sector, making cost control, pricing discipline and strategic positioning central to performance.

Revenue growth masks subdued underlying demand

The group’s 2025 performance reflects a familiar pattern seen across the UK building products sector: reported growth supported by acquisition, but limited underlying momentum.

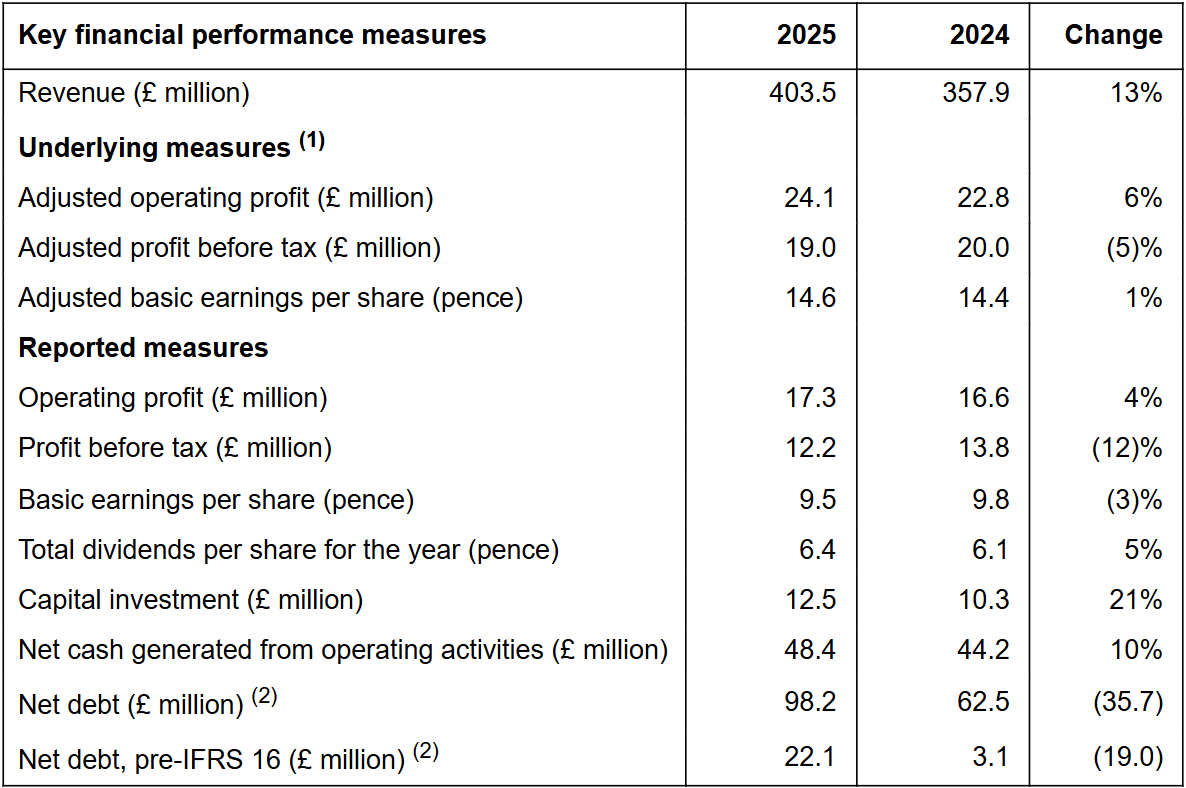

In the first half, revenue increased 10% to £193.2m, but was flat on an organic basis, with volumes down 2%. This dynamic is indicative of wider market conditions—where pricing and bolt-on acquisitions are compensating for weaker end-market demand rather than genuine expansion.

For the full year, this trend is likely to have persisted. The contribution from Alunet (acquired in 2025) will have provided a meaningful uplift to group sales, but underlying activity in core PVC-U systems and RMI channels remained soft. This aligns with earlier trading commentary highlighting subdued residential construction and cautious consumer spending.

Margin improvement a key positive lever

One of the more encouraging aspects of Eurocell’s performance is margin resilience. Preliminary indications show gross margin improving to 52.6% (from 50.9%) , suggesting that the company has continued to execute effectively on pricing, mix and cost control.

This is particularly notable given:

-

Ongoing labour cost inflation

-

Input cost volatility earlier in the year

-

Operational investment (including IT and branch network expansion)

The ability to expand margin in a declining volume environment points to disciplined commercial management and a structurally improving product mix—likely supported by higher-value aluminium systems via Alunet.

Profitability impacted by investment and financing costs

Despite margin gains, profitability has been under pressure.

At the half-year stage:

-

Adjusted operating profit rose 9%

-

Adjusted PBT fell 3%

-

Reported PBT declined sharply (down 50%) due to non-underlying costs and higher finance charges

This reflects three key factors that have likely continued into the full year:

-

Acquisition-related costs – integration expenses and deal-related charges

-

Higher debt levels – net debt increased significantly following the Alunet acquisition

-

Strategic investment – including IT transformation and operational restructuring

The net effect is a divergence between underlying operational progress and statutory earnings, which may temper investor sentiment in the short term.

Alunet acquisition: strategic pivot towards aluminium

The acquisition of Alunet represents a strategically important move for Eurocell, signalling a shift toward aluminium systems and premium product categories.

Its impact in 2025 can be assessed across three dimensions:

1. Revenue diversification

Alunet has provided immediate top-line support, offsetting stagnation in core PVC-U volumes. This diversification reduces reliance on traditional RMI demand, which has been cyclical and currently weak.

2. Margin enhancement potential

Aluminium systems typically command higher margins than commoditised PVC-U products. Early contribution to profit in H1 (supporting adjusted operating growth) suggests the acquisition is earnings-accretive at an operational level.

3. Balance sheet pressure

The downside is increased leverage. Net debt rose materially in H1 2025, reflecting acquisition funding and deferred consideration. In a higher interest rate environment, this introduces an ongoing financing cost drag.

Overall, Alunet appears strategically sound, but its full value will depend on successful integration and sustained demand for aluminium products in a still-fragile market.

Cash flow and capital allocation

Cash generation has softened, with operating cash flow down year-on-year in the first half. This reflects:

-

Working capital outflows

-

Acquisition-related payments

-

Continued capital investment

Eurocell has maintained shareholder returns through dividends and buybacks earlier in the year, but the sustainability of this approach may be increasingly tied to deleveraging priorities.

Sector context: performance better than headline suggests

Context is critical. The UK construction and RMI markets in 2025 have remained under pressure due to:

-

High interest rates suppressing housing transactions

-

Weak consumer confidence impacting discretionary home improvements

-

Limited new build activity

Within this environment, Eurocell’s ability to:

-

Grow reported revenue

-

Expand gross margins

-

Deliver stable underlying operating profit

…represents a relatively robust performance versus peers.

Outlook: recovery dependent on market stabilisation

Looking ahead, Eurocell’s trajectory will be shaped by three variables:

-

Market recovery: Any improvement in housing transactions and RMI demand would provide operational leverage

-

Integration execution: Realising synergies and growth from Alunet will be key to earnings progression

-

Balance sheet management: Reducing leverage to mitigate interest costs

Conclusion

Eurocell’s FY2025 results reflect a business navigating a cyclical downturn with operational discipline and strategic intent.

-

Strengths: Margin expansion, acquisition-led growth, cost control

-

Weaknesses: Weak organic demand, higher debt, pressure on statutory profits

-

Strategic positioning: Strengthened through diversification into aluminium

In summary, Eurocell has delivered a resilient performance in adverse conditions, but the quality of earnings remains influenced by external market weakness and internal investment cycles. The success of its strategy—particularly the Alunet acquisition—will become clearer as market conditions stabilise and integration benefits mature.

Subscribe for FREE below to receive the weekly DGBulletin newsletter and monthly digital magazine!

{kind=link}

{kind=link}

{kind=link}

{kind=link}