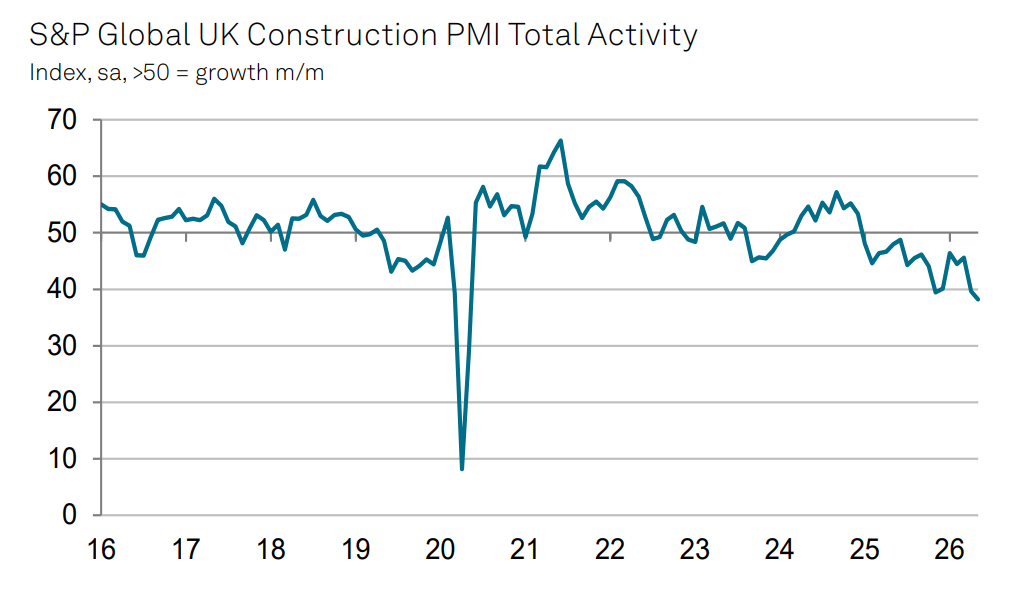

The latest S&P Global UK Construction PMI paints an increasingly bleak picture for the UK construction sector, with output levels falling to their weakest point in six years and housebuilding once again acting as a major drag on overall activity. The data confirms what many across the wider supply chain — including the fenestration sector — have been experiencing for months: delayed projects, weak order books, squeezed margins and growing uncertainty about the pace of recovery.

The headline construction PMI remained deep in contraction territory during the latest reporting period, with civil engineering and residential construction suffering particularly steep declines. Housebuilding activity was among the weakest-performing categories, highlighting the ongoing fragility of the UK housing market and the lack of momentum behind new residential development.

For the UK glazing and fenestration sector, this matters enormously. Residential construction remains one of the most important drivers of demand for windows, doors, curtain walling and associated building envelope products. When housing output contracts at this scale, the slowdown inevitably cascades through fabricators, installers, systems companies and the broader supply chain.

A Perfect Storm Of Construction Headwinds

The latest PMI data is not the result of a single isolated issue. Instead, it reflects a combination of economic, political and structural pressures that have steadily intensified over the past 18 months.

Credit: S&P Global

High borrowing costs continue to weigh heavily on developers and homebuyers alike. Although interest rates have eased slightly from peak levels, financing costs remain materially higher than the ultra-low-rate environment that fuelled previous housebuilding growth. Developers are still facing subdued buyer demand, slower reservation rates and tighter lending conditions.

At the same time, construction firms continue to battle elevated operating costs. Energy, transport and raw material inflation remain problematic, with geopolitical instability adding fresh pressure to already fragile supply chains. Recent reports linked rising fuel and logistics costs directly to worsening conditions across UK construction and manufacturing.

Labour shortages also remain a significant constraint. The industry continues to struggle with an ageing workforce, skills shortages and reduced labour mobility following Brexit. Even where demand exists, many contractors are still unable to scale output efficiently or competitively.

Overlaying all of this is a broader confidence problem. Developers and investors remain cautious about committing to large-scale projects amid uncertain economic growth, fragile consumer confidence and ongoing questions around government policy delivery. The PMI survey highlighted weak pipelines of new work and subdued business optimism across the sector.

What This Means For The Fenestration Sector

For the fenestration industry, the latest downturn reinforces the reality that the sector is now heavily reliant on replacement and retrofit activity rather than buoyant new-build demand.

New housing starts have slowed significantly, meaning fewer opportunities for volume supply into residential developments. This is particularly challenging for companies with heavy exposure to national housebuilders and large residential frameworks.

Commercial construction has also weakened, although not as sharply as residential work. That means commercial glazing specialists are not entirely insulated from the downturn either.

The immediate impact for fenestration businesses is likely to include:

- Increased pricing pressure as competition for fewer projects intensifies

- Longer sales cycles and delayed project approvals

- Greater focus on operational efficiency and cost control

- More consolidation across the supply chain

- Increased dependence on retrofit, refurbishment and energy-efficiency work

There are already signs that many businesses are pivoting toward refurbishment-led demand, particularly as homeowners prioritise improving energy performance over moving house altogether. This trend may provide some insulation for parts of the glazing sector, especially businesses operating within energy-efficient replacement products and retrofit solutions.

However, retrofit alone is unlikely to fully offset the decline in large-scale new-build demand if housing activity continues to weaken.

The 1.5 Million Homes Target Looks Increasingly Unrealistic

The latest construction figures also raise serious questions about the UK government’s ability to achieve its highly ambitious target of delivering 1.5 million new homes during the current parliament.

To hit that figure, the UK would need to sustain annual delivery rates at levels significantly above current output. Yet the PMI data suggests the industry is moving in the opposite direction entirely.

Residential construction has now been one of the weakest-performing segments for a prolonged period, with output repeatedly contracting month after month.

The scale of the challenge goes beyond planning reform alone. Even if planning approvals accelerate, the industry still faces major constraints around:

- Development viability

- Labour availability

- Infrastructure capacity

- Financing costs

- Build cost inflation

- Supply chain resilience

Many developers are also intentionally slowing build-out rates in response to softer demand and affordability pressures in the housing market. There is little incentive to flood the market with new supply when buyer confidence remains fragile, and mortgage affordability continues to suppress transaction volumes.

The government has repeatedly positioned planning reform as the primary mechanism for unlocking housing growth, but the latest PMI data demonstrates that the obstacles are far broader and more systemic.

Without stronger economic growth, improved buyer confidence and materially lower financing costs, construction output is unlikely to recover quickly enough to put the 1.5 million homes target back on track.

Signs Of Stabilisation Remain Limited

Perhaps most concerning in the latest PMI release is the continued weakness in sentiment across the sector. Construction businesses are not simply reporting declining workloads; they are also expressing limited confidence about near-term recovery prospects.

Employment levels across construction have also continued to fall as firms attempt to manage weaker demand and protect margins. That creates an additional long-term risk for the sector, as workforce losses during downturns often create even greater capacity problems during eventual recoveries.

For the glazing and fenestration sector, the near-term environment is therefore likely to remain highly competitive and operationally challenging.

Businesses with strong exposure to social housing retrofit, energy-efficiency upgrades, public sector refurbishment and specialist commercial work may prove more resilient than those heavily dependent on speculative residential development.

At the same time, the longer-term structural drivers behind fenestration demand — decarbonisation, thermal efficiency improvements, Future Homes Standard requirements and ageing housing stock — remain intact.

The problem is that these drivers are currently being overwhelmed by a construction sector facing one of its most difficult trading environments since the pandemic era.

Unless confidence returns quickly and housing activity stabilises, the latest PMI figures may prove to be less of a temporary slowdown and more of a warning sign that the UK construction market is entering a much longer period of subdued activity.

Subscribe for FREE below to receive the weekly DGBulletin newsletter and monthly digital magazine!

{kind=link}

{kind=link}

{kind=link}

{kind=link}