Everest was today sold to Better Capital PCC.

I had news a few months ago that Everest were in a bad way, but, as I have learned from previous misgivings and threats, I decided to keep quiet with this one as I couldn’t find much information to back up that rumour. But as with most rumours, there’s no smoke without fire.

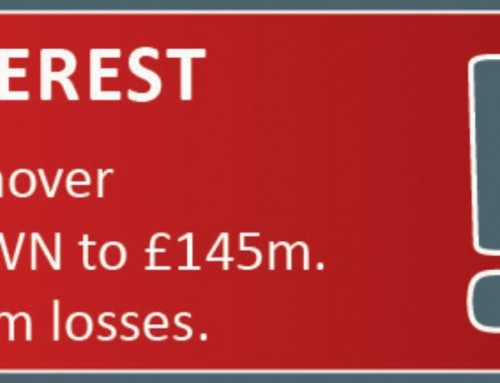

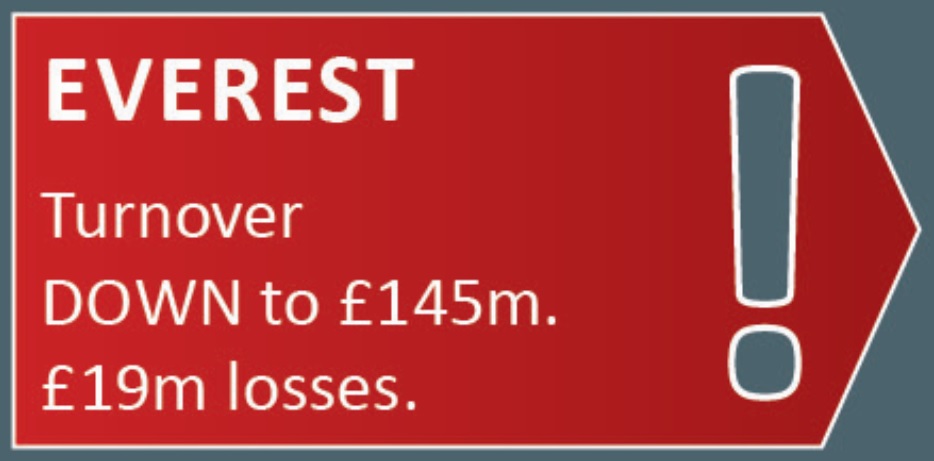

I had been told that Everest had been in bad shape last year, after pretty impressive 2010 revenues of £173 million. However sales may have seen a bit of a nose dive since then, leaving the company in a less than comfortable.

As this news is quite fresh, there is very little known about the purchase itself, other than that Better Capital PCC has purchased 95% of the business, leaving 5% to some original investors.

There has been no comment yet as to whether there will be any job losses or restructuring of the business, but I’m that this sort of information will come out in due course.

Everest has obviously been bought to save the company from worse troubles, and that is clearly a good thing. But my one gripe with these sorts of purchases is that these private equity companies I don’t believe are the best types of companies to run double glazing businesses due to their lack of experience in that industry. In my eyes, for a struggling window company to get back to better times, they should be bought/run by a similar company to make sure any valuable experience and expertise can be passed on and used productively. These capital investment firms are only interested in profit, and if profit isn’t being made, they sell the business and things go down hill from there.

I have made an inquiry to try and find out some more info on the deal. If I get any more reportable information then I shall post it on here ASAP!

{kind=link}

Hi There

iI was a branch manager at Everest .my spies in the camp told me before the takeover they were making people redundant wholesae. To be brutally honest most of the people they got shut of were either deadwood or just salary takers.

Everest is no longer the best sadly . I worked there for 14 yrs in the glory days when the customer was king and not bottomline.

Is there moral there somewhere ?

More will follow.Large overheads definite no no in current climate.

They have already closed the business centre at leeds where i was based its just a depot now

at least 4 office staff 2 surveyors a nd 2 managers went from there and quite a few installation teams

With the horror stories that I have heard regarding their selling techniques I’m surprisedthey have kept going this long.

Say or think what you will but seeing any of the large players in our industry in trouble spells trouble for us all. Despite the bad press that they inevitably attract, they have spent a lot of money on promoting double (and triple) glazing through all types of media including the TV and that benefits us all. They have also (in most cases) been at the forefront of many of the product improvements and have helped fight off damaging legislation which would have damaged our industry. You may not like some of their tactics but we would be a much… Read more »

Hi Mark

I recently championed Everest’s latest TV adverts as helping the industry create a classier image. Their ads a better than most and do a lot of good for our industry. I don’t think anyone wishes to see a national go as they help generate business for the rest of the industry.

I certainly don’t like their hard sell tactics or ridiculous discounts, but their presence in the industry ensures our sector still has some clout!

DGB

Phil why did you leave everest.According to my spies you were well rotton wood.

yeh yeh course i was . mark warren is correct in his observations. everest paved the way from the mid 60,s . i was actually well acquainted with arnold bird , josh manches and frank shaw from the glory days. i ve probably forgotten more about everest than you ever knew , oh and i knew ted moult god rest his soul the motto at leeds wasnt fit the best fit everest , it was fit wat ever you can get away with fit everest . oh the reason why i left a culture of bullying and racism which senior… Read more »

having said that i hope the new management team at everest can turn around its fortunes and make it number 1 again. by the way give us a job !!!!

Only jokin phill.They are a rancid outfit to work for.Its a pity you cant private message on here ive loads on them

thats kool . nothing personal lol you had to be there to believe it. luckily those involved got their come uppance when the business centre closed. good riddance to bad rubbish