In the business world it has been earnings season for the last couple of weeks or so, and in the window world this is no different. Eurocell is the next name to publish it’s half-year report, and on the face of it, all seems to be going rather well.

The overview

I’m not going to rake through the whole report on here, it’s a solid 25 pages long and I’m sure you all have important things to be getting on with. If you do have the spare time however and you want to go through the whole report you can follow this link: https://www.eurocell.co.uk/news/positive-half-year-results

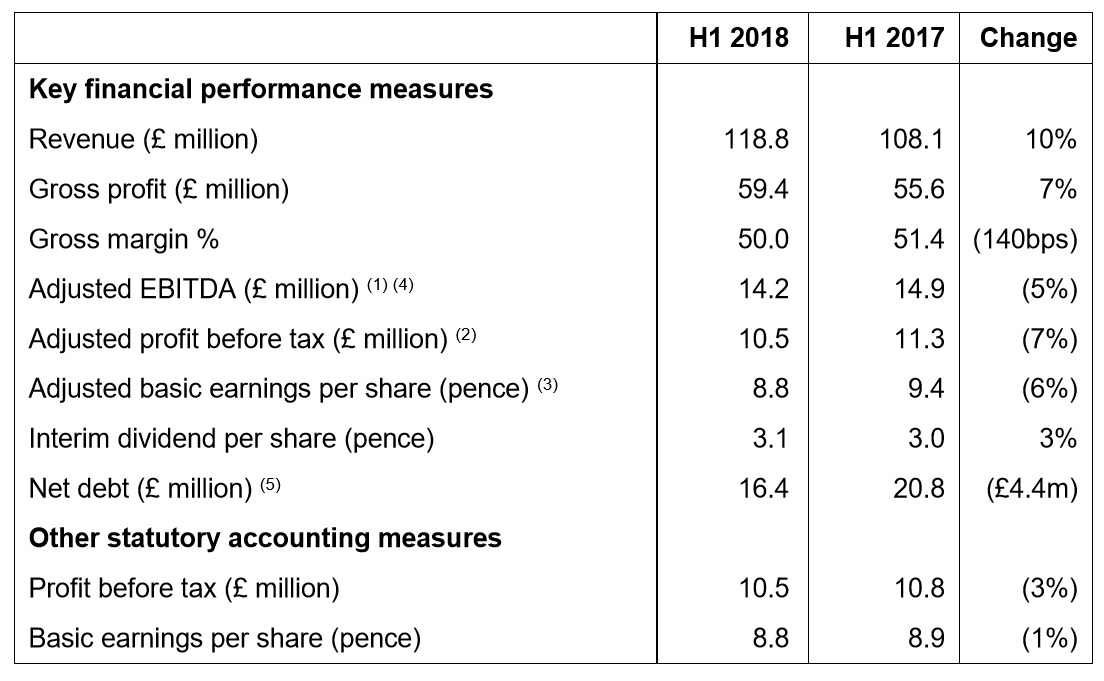

These are the stats that matter:

Credit: Eurocell

On a percentage basis, all up, apart from gross margin. But given the pressures on raw material costs, wage costs, acquisitions and new branch openings, we can forgive them 1.4%. Plenty of us in the sector would love a 50% gross margin!

What has stuck out for me was their net debt. Down a whopping £4.4m compared to the first half of last year. This to me says that they are making hay while the sun shines and paying down what they owe while they can afford to easily do so. There is a slowdown coming, so it makes total sense to be offloading their debt at this moment in time.

The other stats that stand out for me are their increased revenues. A 10% change is very healthy indeed, and would indicate some level of market share increase. Not all systems companies are booming in the same way, but it has been because of their diversification and their ability to be able to serve almost all areas of fenestration which has helped them see revenues rise healthily.

Gross profit is up 7%. That is pretty impressive for me. We’re facing an environment of rising costs, slowing growth and an overall challenging marketplace. To squeeze out another 7% of profit from what has been a very tough H1 is good going.

I’m not going to repeat every stat to you, you can read, and you can read the full page report by clicking the link above.

Positive position

When you look at the share price of Eurocell, it is one of the best performing fenestration related stocks out there. It’s not far from it’s all-time highs of 268p, sitting currently at 259p per share and with a market cap of just shy of £338m. I have said in the past that Eurocell have done a very good job in diversifying their offering to the whole of the supply chain. This puts them in a very positive position right now.

Eurocell currently find themselves in a very strong market position right now. Not because of one single product, but because of their massive spread across the market. They are ahead of many on the recycling front and green initiatives. They have a huge network of trade centres up and down the UK. They have an already established portfolio of window and door products, including their Skypods, Aspect bi-folds and now an aluminium offering. They are all things to all people, and generally have a good reputation when it comes to service.

How many other systems companies can boast the same USPs? Not many. This is what puts Eurocell in a very strong position as we head into H2. They could quite easily eat up plenty of market share from their competitors in the coming months. On the recycling front it’s really only VEKA that are as established as they are right now. The rest do seem to be lagging behind.

So, onwards and upwards for Eurocell. Can the others keep up the pace?

To get weekly updates from DGB sent to your inbox, enter your email address in the space below to subscribe:

By subscribing you agree to DGB sending you weekly email updates with all published content on this website, as well as any major updates to the services being run on DGB. Your data is never passed on to third parties or used by external advertising companies. Your data is protected and stored on secure servers run by Fivenines UK Ltd.

{kind=link}

{kind=link}

{kind=link}

{kind=link}